Volume Weighted Trend (VWT)

Minimum bars needed: vwma_length bars

(default params: 34 bars (vwma_length=34))

The VWMA needs vwma_length bars of price and volume data. The ATR band also uses the same period. After warmup, the indicator updates in real-time.

✅ After the warmup window is filled, this indicator produces a new value on every incoming bar in real-time.

The VWMA center line and trend signals lag behind price reversals.

| Event | Lag | Detail |

|---|---|---|

| VWMA center line reacts to price reversal | ≈ vwma_length / 2 bars | VWMA has lag ≈ vwma_length/2 |

| Upper/lower bands react | ≈ vwma_length / 2 bars | Bands use ATR with same period as VWMA |

| Trend flips bullish ↔ bearish | ≈ vwma_length / 2 bars | Trend determined by close vs VWMA |

| Buy / sell signal fires | ≈ vwma_length / 2 bars | Signal fires on the bar the trend flips |

Formula for custom params: lag ≈ vwma_length / 2

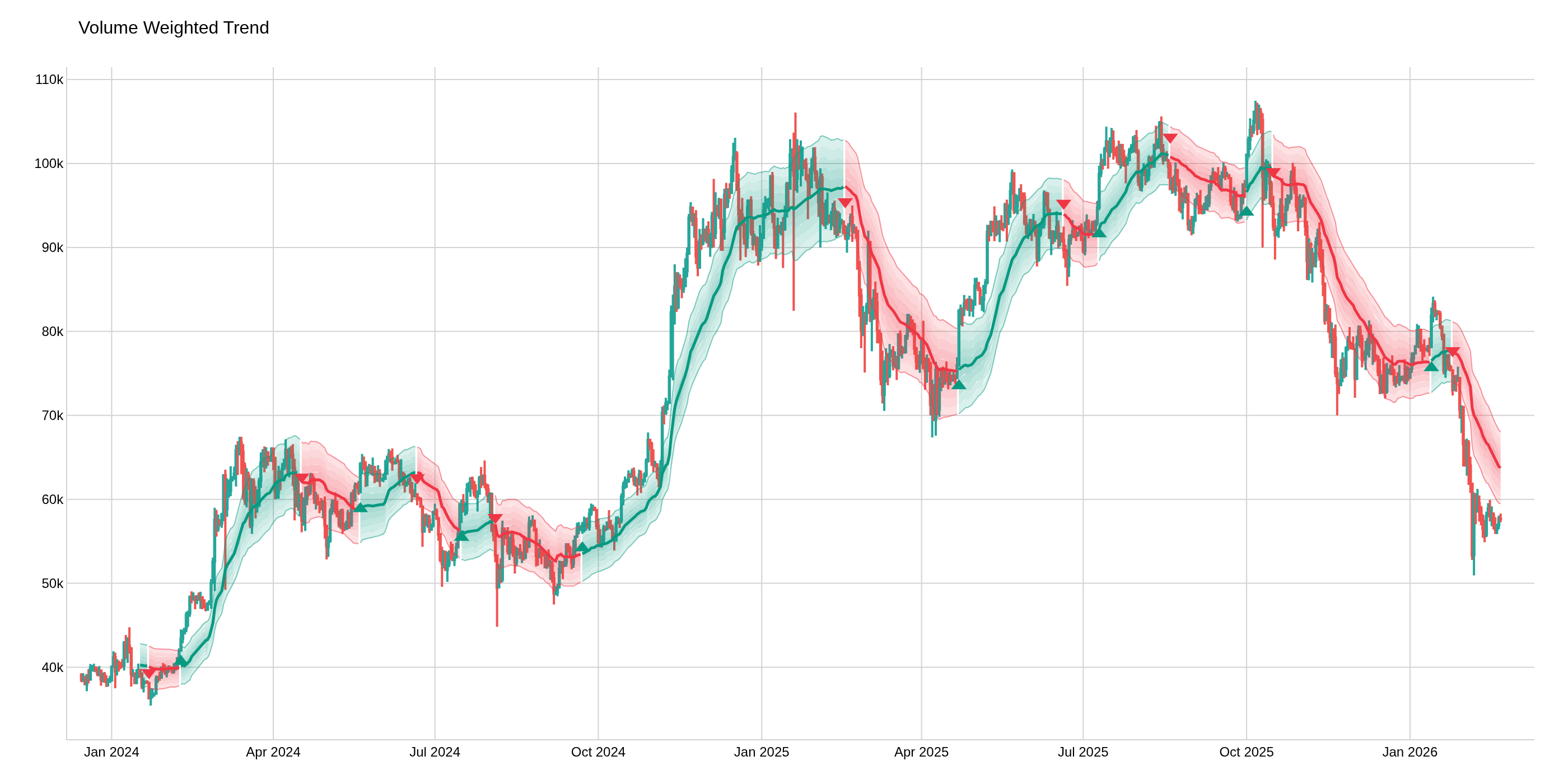

The Volume Weighted Trend indicator uses a Volume Weighted Moving Average (VWMA) with ATR-based volatility bands to determine trend direction. Based on the "Volume Weighted Trend [QuantAlgo]" concept. The VWMA serves as the trend baseline, while upper and lower bands (VWMA +/- ATR * multiplier) define breakout thresholds. The trend flips bullish when price closes above the upper band and bearish when price closes below the lower band.

def volume_weighted_trend(

df: Union[PdDataFrame, PlDataFrame],

vwma_length: int = 34,

atr_multiplier: float = 1.5,

high_column: str = "High",

low_column: str = "Low",

close_column: str = "Close",

volume_column: str = "Volume",

) -> Union[PdDataFrame, PlDataFrame]:

Returns the following columns:

vwt_vwma: Volume Weighted Moving Averagevwt_atr: Average True Rangevwt_upper: Upper volatility band (VWMA + ATR * multiplier)vwt_lower: Lower volatility band (VWMA - ATR * multiplier)vwt_trend: Trend direction (+1 bullish, -1 bearish, 0 undefined)vwt_trend_changed: 1 on bars where trend flipped, 0 otherwisevwt_signal: +1 on bullish flip, -1 on bearish flip, 0 otherwise

Example

from investing_algorithm_framework import download

from pyindicators import volume_weighted_trend, get_volume_weighted_trend_stats

pd_df = download(

symbol="btc/eur",

market="bitvavo",

time_frame="4h",

start_date="2024-01-01",

end_date="2024-04-01",

pandas=True,

)

# Calculate Volume Weighted Trend

pd_df = volume_weighted_trend(pd_df, vwma_length=34, atr_multiplier=1.5)

# Get summary statistics

stats = get_volume_weighted_trend_stats(pd_df)

print(stats)

pd_df[["Close", "vwt_vwma", "vwt_upper", "vwt_lower", "vwt_trend", "vwt_signal"]].tail(10)

Momentum and Oscillators

Indicators that measure the strength and speed of price movements rather than the direction.

The image above uses the following parameters:

| Parameter | Value |

|---|---|

vwma_length | 34 |

atr_multiplier | 1.5 |