Zero-Lag EMA Envelope (ZLEMA)

Minimum bars needed: length bars

(default params: 200 bars (length=200))

The ZLEMA center line needs length bars to initialize. The ATR bands additionally need atr_length bars. After warmup, both update in real-time.

✅ After the warmup window is filled, this indicator produces a new value on every incoming bar in real-time.

The center line has near-zero lag; the ATR-based bands still lag.

| Event | Lag | Detail |

|---|---|---|

| Center line reacts to price reversal | ≈ 0 bars | ZLEMA compensates EMA lag via close + (close − close[lag]) |

| Upper/lower bands react to volatility change | ≈ atr_length / 2 bars | Bands are offset by ATR; ATR smoothing introduces lag of atr_length / 2 |

Formula for custom params: center ≈ 0; bands ≈ atr_length / 2

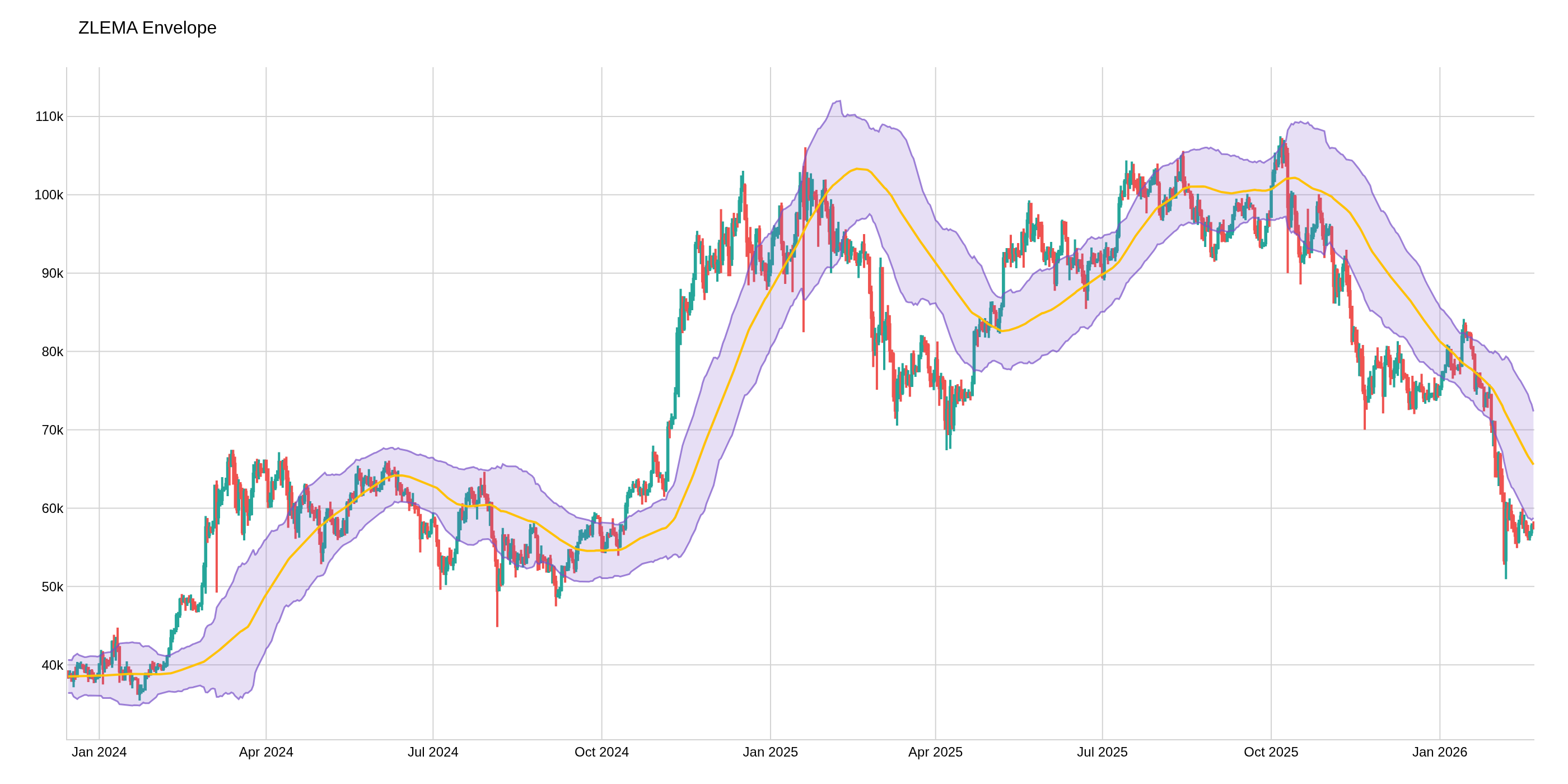

The Zero-Lag EMA Envelope combines a Zero-Lag Exponential Moving Average (ZLEMA) with ATR-based bands and multi-bar swing confirmation. The ZLEMA compensates for the inherent lag of a standard EMA by using a lag-compensated source (close + (close - close[lag])). Trend state is confirmed when multiple consecutive bars close beyond a band while the ZLEMA slope agrees.

Calculation:

lag = floor((length - 1) / 2)compensated = close + (close - close[lag])ZLEMA = EMA(compensated, length)Upper = ZLEMA + ATR × multLower = ZLEMA - ATR × mult- Bull: close > Upper for N bars AND ZLEMA rising

- Bear: close < Lower for N bars AND ZLEMA falling

def zero_lag_ema_envelope(

data: Union[PdDataFrame, PlDataFrame],

source_column: str = 'Close',

length: int = 200,

mult: float = 2.0,

atr_length: int = 21,

confirm_bars: int = 2,

upper_column: str = 'zlema_upper',

lower_column: str = 'zlema_lower',

middle_column: str = 'zlema_middle',

trend_column: str = 'zlema_trend',

signal_column: str = 'zlema_signal',

) -> Union[PdDataFrame, PlDataFrame]:

Example

from investing_algorithm_framework import download

from pyindicators import zero_lag_ema_envelope

pl_df = download(

symbol="btc/eur",

market="binance",

time_frame="1d",

start_date="2023-12-01",

end_date="2023-12-25",

save=True,

storage_path="./data"

)

pd_df = download(

symbol="btc/eur",

market="binance",

time_frame="1d",

start_date="2023-12-01",

end_date="2023-12-25",

pandas=True,

save=True,

storage_path="./data"

)

# Calculate Zero-Lag EMA Envelope for Polars DataFrame

pl_df = zero_lag_ema_envelope(pl_df, source_column="Close", length=200, mult=2.0)

pl_df.show(10)

# Calculate Zero-Lag EMA Envelope for Pandas DataFrame

pd_df = zero_lag_ema_envelope(pd_df, source_column="Close", length=200, mult=2.0)

pd_df.tail(10)

The image above uses the following parameters:

| Parameter | Value |

|---|---|

source_column | Close |

length | 200 |

mult | 2.0 |