Average True Range (ATR)

Warmup Window

Minimum bars needed: period bars

(default params: 14 bars (period=14))

Wilder's RMA needs period bars for the initial average true range. After warmup, ATR updates in real-time on every new bar.

✅ After the warmup window is filled, this indicator produces a new value on every incoming bar in real-time.

Lagging Indicator

ATR readings lag behind actual volatility changes.

| Event | Lag | Detail |

|---|---|---|

| ATR reacts to a volatility spike | ≈ period / 2 bars | Wilder's RMA smoothing over the specified period |

| ATR reacts to volatility contraction | ≈ period / 2 bars | Same smoothing; contractions are also detected late |

Formula for custom params: lag ≈ period / 2

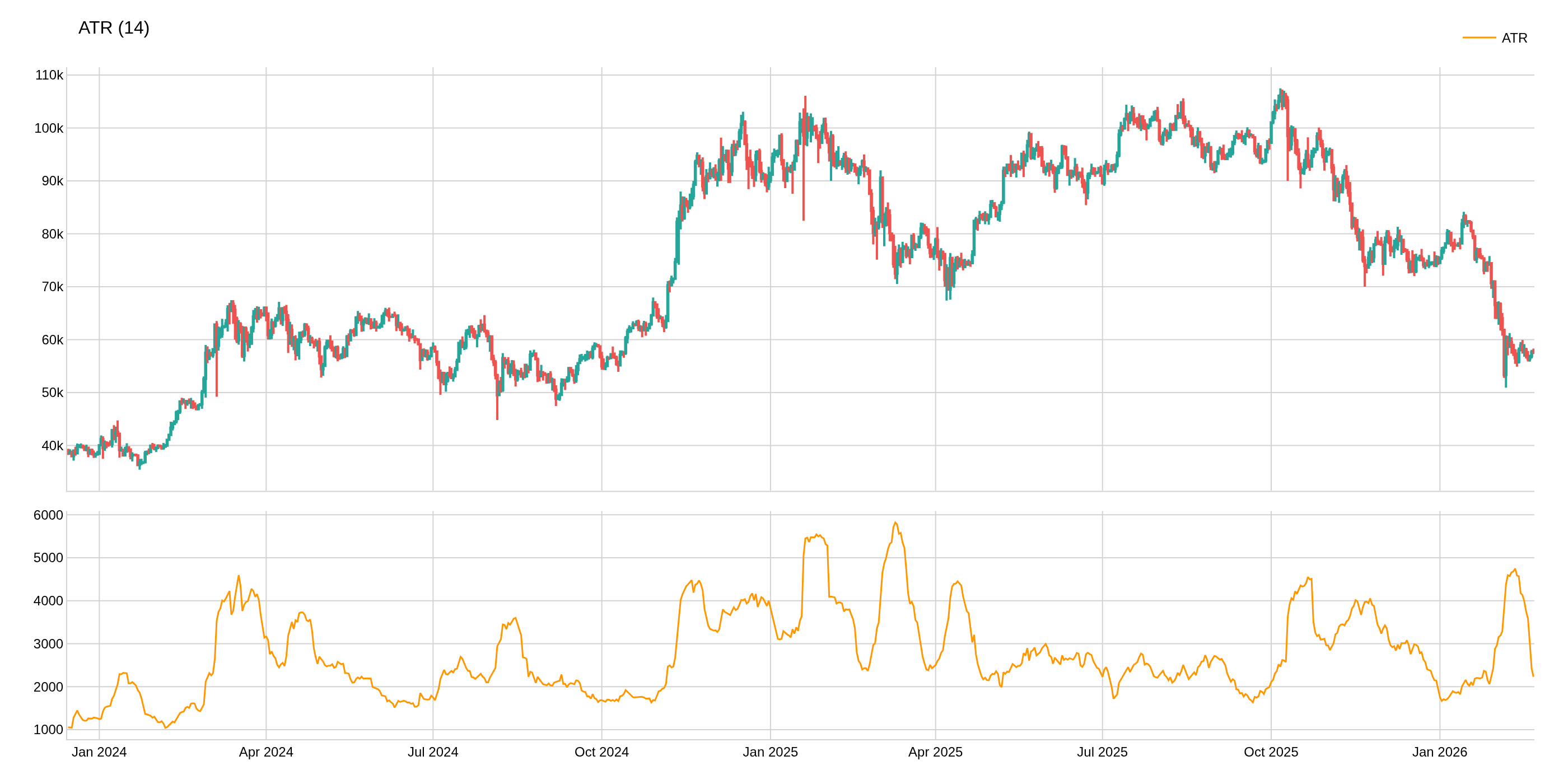

The Average True Range (ATR) is a volatility indicator that measures the average range between the high and low prices over a specified period. It helps traders identify potential price fluctuations and adjust their strategies accordingly.

def atr(

data: Union[PdDataFrame, PlDataFrame],

source_column="Close",

period=14,

result_column="ATR"

) -> Union[PdDataFrame, PlDataFrame]:

Example

from investing_algorithm_framework import download

from pyindicators import atr

pl_df = download(

symbol="btc/eur",

market="binance",

time_frame="1d",

start_date="2023-12-01",

end_date="2023-12-25",

save=True,

storage_path="./data"

)

pd_df = download(

symbol="btc/eur",

market="binance",

time_frame="1d",

start_date="2023-12-01",

end_date="2023-12-25",

pandas=True,

save=True,

storage_path="./data"

)

# Calculate average true range for Polars DataFrame

pl_df = atr(pl_df, source_column="Close")

pl_df.show(10)

# Calculate average true range for Pandas DataFrame

pd_df = atr(pd_df, source_column="Close")

pd_df.tail(10)

Chart Parameters

The image above uses the following parameters:

| Parameter | Value |

|---|---|

source_column | Close |

period | 14 |